5.3 Understand The Methods Used To Account For Uncollectible ...

Maybe your like

Direct write-off method

The direct write-off method delays recognition of bad debt until the specific customer accounts receivable is identified. Once this account is identified as uncollectible, the business will record a reduction to the customer’s accounts receivable and an increase to bad debt expense for the exact amount uncollectible.

Under generally accepted accounting principles (GAAP), the direct write-off method is not an acceptable method of recording bad debts, because it violates the matching principle. For example, assume that a credit transaction occurs in September 2021 and is determined to be uncollectible in February 2022. The direct write-off method would record the bad debt expense in 2022, while the matching principle requires that it be associated with a 2021 transaction, which will better reflect the relationship between revenues and the accompanying expenses. This matching issue is the reason accountants will typically use one of the two accrual-based accounting methods introduced to account for bad debt expenses.

It is important to consider other issues in the treatment of bad debts. For example, when a business accounts for bad debt expenses in their financial statements, it will use an accrual-based method; however, they are required to use the direct write-off method on their income tax returns. This variance in treatment addresses taxpayers’ potential to manipulate when a bad debt is recognised. Because of this potential manipulation, the Australian Taxation Office (ATO) requires that the direct write-off method must be used when the debt is determined to be uncollectible, while GAAP still requires that an accrual-based method be used for financial accounting statements.

For the taxpayer, this means that if a business sells an item on credit in October 2021 and determines that it is uncollectible in June 2022, it must show the effects of the bad debt when it files its 2022 tax return. This application probably violates the matching principle, but if the ATO did not have this policy, there would typically be a significant amount of manipulation on company tax returns. For example, if the business wanted the deduction for the write-off in 2021, it might claim that it was actually uncollectible in 2021, instead of in 2022. This method also does not provide the best estimate of how accounts receivable affect expected cash inflow for the business.

The final point relates to businesses with very little exposure to the possibility of bad debts, typically, entities that rarely offer credit to its customers. Assuming that credit is not a significant component of its sales, these sellers can also use the direct write-off method. The companies that qualify for this exemption, however, are typically small and not major participants in the credit market. Thus, virtually all of the remaining bad debt expense material discussed here will be based on an allowance method that uses accrual accounting, the matching principle, and the revenue recognition rules under GAAP.

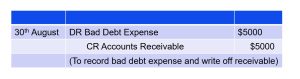

For example, assume Kenco makes a $5000 credit sale to Bennards on 28th March. On 30th August, Kenco Ltd determines that it will be unable to collect from Bennards. When the account defaults for non-payment on 30th August, Kenco would record the following journal entry to recognise bad debt.

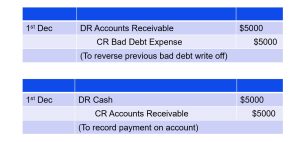

Bad Debt Expense increases (debit), and Accounts Receivable decreases (credit) for $5000. If, in the future, any part of the debt is recovered, a reversal of the previously written-off bad debt, and the collection recognition is required. Let’s say this customer unexpectedly pays in full on 1st December, the business would record the following journal entries:

Bad Debt Expense increases (debit), and Accounts Receivable decreases (credit) for $5000. If, in the future, any part of the debt is recovered, a reversal of the previously written-off bad debt, and the collection recognition is required. Let’s say this customer unexpectedly pays in full on 1st December, the business would record the following journal entries:

The first entry reverses the bad debt write-off by increasing Accounts Receivable (debit) and decreasing Bad Debt Expense (credit) for the amount recovered. The second entry records the payment in full with Cash increasing (debit) and Accounts Receivable decreasing (credit) for the amount received of $5000.

The first entry reverses the bad debt write-off by increasing Accounts Receivable (debit) and decreasing Bad Debt Expense (credit) for the amount recovered. The second entry records the payment in full with Cash increasing (debit) and Accounts Receivable decreasing (credit) for the amount received of $5000.

As you’ve learned above, the delayed recognition of bad debt violates GAAP, specifically the matching principle. Therefore, the direct write-off method is not used for publicly listed companies; the allowance method is used instead.

Allowance method

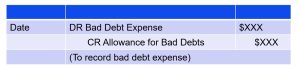

The allowance method is the more widely used method because it satisfies the matching principle. The allowance method estimates bad debt during a period, based on certain computational approaches. The calculation matches bad debt with related sales during the period. The estimation is made from past experience and industry standards. Essentially, the allowance method splits the accounting into two entries, firstly an entry to record an estimate of bad debt expense and secondly an entry to write off receivables when they become uncollectible. When the estimation is recorded at the end of a period, the following entry occurs:

The journal entry for the Bad Debt Expense increases (debit) the expense balance, and the Allowance for Doubtful Accounts increases (credit) the balance in the Allowance. When setting up the allowance, the allowance account is a contra asset account, and is subtracted from Accounts Receivable to determine the Net Realisable Value of the Accounts Receivable account on the balance sheet. This means that when it is subtracted from Accounts Receivable, the difference represents an estimate of the cash value of accounts receivable. The contra account may also be called the Provision for Bad Debts or the Allowance for Bad Debts in practice.

Tag » When Does An Account Become Uncollectible

-

Accounts Uncollectible Definition - Investopedia

-

What Is An Uncollectible Account And When Does It Become ...

-

When Does An Account Become Uncollectible? - First Credit Services

-

When Does An Account Become Uncollectible?

-

Business Owners: When Does An Account Become Uncollectible?

-

ACCOUNTING CHAPTER 8 FINAL Flashcards - Quizlet

-

Evaluating Accounts Receivable - Cliffs Notes

-

Allowance For Doubtful Accounts And Bad Debt Expenses

-

Solved Question 17 2 Pts When Does An Account Become

-

7.2 Accounting For Uncollectible Accounts

-

When Does An Account Become Uncollectible A When The

-

How Do You Write Off A Bad Account? | AccountingCoach

-

Allowance For Doubtful Accounts - Overview, Guide, Examples

-

How Can A Business Protect Against Uncollectible Accounts?